Ethereum Staking APR Snapshot: May 2026

Ethereum staking APR in May 2026 sits across a clearly defined spectrum, with yields ranging from 2.1% for custodial exchange products to approximately 5% for technically sophisticated solo validators. The Compass Staking Yield Reference Index (STYETH)—which derives its figures directly from an Ethereum consensus node, bypassing third-party estimation—recorded an annualized daily staking yield of 2.8329% APY as of May 1, 2026, and serves as the institutional standard for measuring pure consensus-layer rewards (source: Compass FT STYETH, 2026-05). A total of 35,859,802 ETH is now staked—28.91% of total supply—secured by over 1.1 million active validators with an aggregate economic value near $112 billion. Net staking inflows turned negative in early January 2026, representing a mild net exit of approximately 600,000 ETH from the validator set, which has partially unwound the yield compression seen throughout 2024–2025. The validator exit queue has simultaneously collapsed to just 32 ETH—a 99.9% reduction from its peak—meaning exits now settle in under one minute. This structural shift matters: lower net staking tends to support slightly higher per-validator yields going forward.

Quick Answer: The Compass STYETH benchmark places Ethereum staking at 2.8329% APY for pure consensus-layer rewards as of May 1, 2026. Retail yields span from roughly 2.1% (Coinbase cbETH, after fees) to ~5% for solo validators using MEV-boost, with 35.86M ETH currently staked—28.91% of total ETH supply.

The year-to-date performance of the STYETH index reads –1.47% through May 1, 2026, reflecting continued long-run yield compression as cumulative staked ETH has grown across multiple years. Even so, the negative flow data from early 2026 introduces a modest counterforce: with validators exiting at a pace that modestly outpaces new entrants, the per-validator share of consensus rewards stabilizes or nudges upward. This dynamic is worth monitoring closely through Q2 2026 as institutional programs reassess their participation rates.

MEV (Maximal Extractable Value) remains the primary variable separating benchmark-rate stakers from high-performing validators. MEV-boost middleware, which allows validators to source pre-built blocks from professional builders, continues to add 1–2 percentage points above the consensus-layer baseline for active operators. On-chain activity levels—DeFi volume, arbitrage frequency, NFT trading—directly correlate with MEV rewards, which means realized yields are not fixed. According to Datawallet's Ethereum Staking Statistics, the economic security value of staked ETH currently sits at approximately $112 billion, underscoring the network's maturity as an institutional-grade asset class with real yield-generating mechanics.

| Platform / Method | Net APY (May 2026) | Fee on Rewards | Custody Model | Minimum Stake | Liquidity |

|---|---|---|---|---|---|

| Solo Staking | 4–5% (with MEV-boost) | 0% | Self-custodied | 32 ETH (~$80K+) | None (withdrawal queue) |

| Lido EarnETH Vault | 3.3% APY | 10% | Non-custodial | Any amount | High (secondary market) |

| Lido (stETH) | 2.6% APY | 10% | Non-custodial | Any amount | Very high (secondary market) |

| ether.fi (eETH + restaking) | ~2.8%+ APY | ~10% | Non-custodial | Any amount | High (secondary market) |

| Rocket Pool (rETH) | 2.19% APY | ~14% | Non-custodial | Any amount (stakers) | High (secondary market) |

| Binance | ~2–3% APY | Variable | Custodial | Any amount | Varies by product |

| Kraken | ~2–2.9% APY | Variable | Custodial | Any amount | Varies by product |

| Coinbase (cbETH) | ~2.1–2.5% APY | ~25% | Custodial | Any amount | Moderate (cbETH token) |

"The STYETH index is derived directly from on-chain Ethereum consensus data, providing a transparent, manipulation-resistant reference rate for institutional products and ETH staking derivatives. As of May 1, 2026, the index reflects a 2.8329% annualized daily staking yield with a year-to-date return of –1.47%, consistent with ongoing structural yield compression." — Compass FT, STYETH Index Methodology

Solo Staking: Highest Yield, Highest Barrier

Solo staking is the yield ceiling for Ethereum participants, offering the full consensus-layer reward with no platform fee deduction. The base consensus-layer return for solo validators stands at approximately 2.84% APY—aligned with the STYETH benchmark—but this figure rises materially when execution-layer rewards are included. According to ChainLabo's 2026 Ethereum Staking Rewards Guide, validators using MEV-boost middleware to source high-value block proposals from professional block builders can realistically achieve 4–5% APY on an annualized basis, with individual epochs occasionally producing outsized returns during periods of elevated on-chain activity. The trade-offs are significant: solo staking demands a 32 ETH minimum (~$80,000+ at current prices), dedicated validator hardware, a reliable high-uptime internet connection, and ongoing technical maintenance. Slashing—the irreversible penalty for validator misconduct or misconfiguration—is a non-trivial risk that operators must actively mitigate through proper key management and client configuration. For holders with long-term conviction, the necessary capital, and genuine technical proficiency, solo staking remains the most economically efficient path available.

The 32 ETH capital barrier is the most significant limiting factor for most retail participants. At current prices this translates to an entry cost well above $80,000—a threshold that makes solo staking inaccessible to the majority of ETH holders regardless of technical skill. This is not a protocol design flaw but a deliberate security mechanism: the 32 ETH requirement creates meaningful economic alignment between validators and network health, since a validator's entire stake is exposed to penalties if they behave incorrectly or maintain poor uptime.

Hardware and operational requirements compound the capital barrier further. A solo validator needs a dedicated machine—or a reliable cloud VPS—running both an execution client (Geth or Nethermind) and a consensus client (Lighthouse or Prysm) continuously. Downtime results in incremental inactivity penalties; double-signing results in slashing, an irreversible reduction of stake that cannot be reversed by the Ethereum protocol. Operators are responsible for private key security, client software updates, and system monitoring. This level of ongoing commitment suits technically proficient participants who treat staking as active infrastructure management, not a passive deposit.

MEV-boost's impact on solo staking yield is substantial and widely underappreciated. Priority fees—paid by users who want their transactions included promptly—and MEV extraction during block proposals account for the entire gap between the 2.84% base consensus rate and the 4–5% realized yield cited for active operators. Professional builder networks including Flashbots and BloXroute compete to include high-value transactions in validator-proposed blocks, and validators connected through MEV-boost capture a larger share of this competition's output. Realized MEV premiums vary with on-chain activity: quiet periods narrow the gap, while periods of elevated DeFi volume or arbitrage activity widen it significantly.

"Solo validators who run MEV-boost and maintain strong uptime can realistically target 4–5% APY in 2026—the highest available yield in the Ethereum staking ecosystem. The trade-off is operational complexity and capital commitment that most retail participants are not positioned to absorb." — ChainLabo, Ethereum Staking Rewards Guide 2026

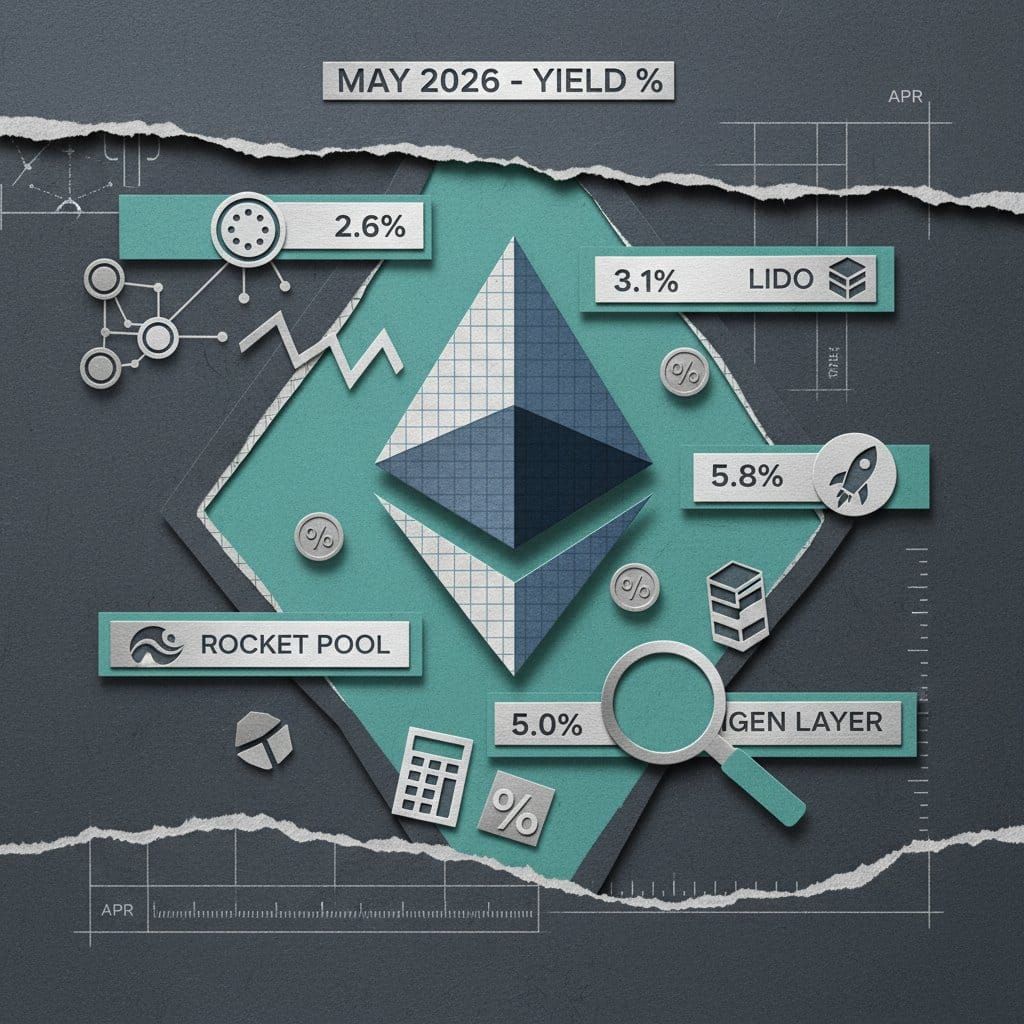

Lido (stETH): Market Leader at 2.6%–3.3% APY

Lido Finance is the dominant force in Ethereum liquid staking, controlling approximately 24.2% of all staked ETH—between 8.7 and 9.1 million ETH depending on the measurement date—with a total value locked of approximately $20.9 billion as of May 2026. Lido's flagship product, stETH, delivers a staking APR of 2.6% as displayed on its homepage after its 10% performance fee is deducted from gross consensus-layer rewards (source: Lido Finance, 2026-05). Since its 2020 launch, Lido has paid out a cumulative $2.65 billion in staking rewards to stETH holders—a figure that underscores the protocol's track record over multiple market cycles. Beyond base staking, Lido offers two yield-enhanced products: the "EarnETH" vault, which deploys stETH across DeFi protocols to target 3.3% APY, and an "EarnUSD" product offering 5.1% APY in USD-denominated terms. This latter figure is an important distinction: EarnUSD is a currency-specific return and should not be compared directly to ETH-denominated staking yields across platforms.

The 10% performance fee positions Lido in the mid-range among major liquid staking providers. Rocket Pool charges approximately 14% to node operators; Coinbase charges roughly 25%. For holders who prioritize simplicity and deep secondary-market liquidity, Lido's fee is a reasonable structure: stETH is one of the most liquid crypto assets on chain, tradeable against ETH on Curve, Uniswap, and Balancer with minimal price impact for typical retail position sizes. This on-chain liquidity makes stETH the default choice for DeFi participants who need to maintain capital flexibility while capturing staking yield.

Lido's market position carries a concentration consideration that the Ethereum community has discussed actively. A single protocol controlling nearly a quarter of staked ETH creates governance and systemic risk at the consensus layer—a validator set that could theoretically coordinate in ways that smaller protocols cannot. Lido addresses this through a permissioned registry of professional node operators distributed across multiple geographies and client implementations, but the concentration debate remains live. For traders and investors primarily focused on yield and liquidity, this does not materially affect day-to-day return; it is, however, a factor for participants who weigh Ethereum network health alongside their personal position.

The EarnETH and EarnUSD products represent Lido's strategic expansion beyond pure staking. EarnETH at 3.3% APY achieves its uplift by deploying stETH as collateral in DeFi money markets and liquidity pools, stacking lending or liquidity fees on top of base consensus rewards. EarnUSD at 5.1% APY is structurally distinct—it is best evaluated as a stablecoin-adjacent product for holders who want USD-denominated yield exposure, not as a measure of ETH staking efficiency. Separating these three products when benchmarking Lido against competitors is essential for an accurate comparison.

Rocket Pool (rETH) and Decentralized Alternatives

Rocket Pool is Ethereum's most accessible permissionless staking infrastructure, allowing any holder to stake any amount of ETH and receive rETH in return, while node operators—who run the underlying validators—can participate with as little as 8 ETH in collateral, down from the previous 16 ETH minimum. The current rETH staking yield stands at 2.19% APY according to StakingRewards.com tracking as of May 2026, placing it slightly below Lido's stated 2.6% base rate. This gap reflects Rocket Pool's fee structure: approximately 14% of consensus rewards are redirected to node operators as compensation for running the infrastructure, with rETH holders receiving the residual share. For participants who treat decentralization and trust-minimization as primary selection criteria alongside yield, Rocket Pool's permissionless architecture is a structurally meaningful differentiator versus Lido's permissioned operator set—any participant meeting the 8 ETH threshold can run a validator without seeking approval from a committee.

The reduction of the node operator minimum from 16 ETH to 8 ETH is a significant protocol evolution. It lowers the capital barrier to running a Rocket Pool minipool substantially, which should incrementally expand the number of independent validators in the network and improve geographic and client diversity. Rocket Pool node operators also hold RPL—the protocol's native governance token—as additional collateral, creating an economic alignment between the staking system and the protocol's native asset. This introduces both an incentive structure for operators and price exposure to RPL for those running minipools, a consideration distinct from rETH holder risk.

rETH's compatibility with EigenLayer restaking introduces an additional yield dimension for participants who want to maximize capital efficiency. Rocket Pool stakers can restake their rETH on EigenLayer, delegating their economic security to Actively Validated Services (AVS) and earning supplemental rewards on top of the 2.19% base rate. The combined yield depends on AVS operator commissions, specific service selection, and market-driven AVS reward rates. For participants already comfortable with Rocket Pool's risk profile, restaking is a logical yield extension that leverages an existing position without requiring migration to a different protocol.

Among other decentralized staking alternatives, Figment deserves recognition as a professional staking-as-a-service provider primarily serving institutional clients. Figment custodies approximately 1,480,352 ETH—4.1% of total staked ETH—and offers SLA-backed uptime guarantees and compliance documentation. Figment is not a consumer-facing liquid staking product but its institutional market share reflects the growing demand for professionally managed validator infrastructure with contractual accountability.

"rETH currently yields 2.19% APY, reflecting Rocket Pool's node operator fee structure and its standing as the leading permissionless liquid staking protocol on Ethereum. For holders who prioritize decentralization over marginal yield optimization, the concession relative to Lido's base rate is the quantifiable cost of a more trust-minimized system." — StakingRewards.com, rETH Asset Analytics

Centralized Exchange Staking: Coinbase, Binance, Kraken

Centralized exchange (CEX) staking represents the lowest-friction, lowest-yield tier of Ethereum staking in May 2026. Coinbase, Binance, and Kraken collectively hold a substantial share of the CEX staking market and offer simplified user experiences at the cost of higher fee extraction and custodial risk. Binance holds the largest CEX position at 3,289,104 ETH—38.74% of the centralized exchange staking market—with rates typically hovering between 2% and 3% APY depending on the product structure selected. Coinbase holds 1,840,952 ETH (21.69% of the CEX market) and charges approximately 25% of staking rewards—the highest fee rate among major platforms—resulting in a net APY of roughly 2.1–2.5% for cbETH holders, making it the lowest net-yield option in this comparison (source: Datawallet Ethereum Staking Statistics). Kraken holds 1,347,650 ETH (15.87% of the CEX market) and offers approximately 2–2.9% APY, positioning it as marginally more competitive on yield within the CEX tier despite a smaller absolute staking base.

The premium paid for CEX staking is fundamentally an accessibility premium—it does not translate into reduced risk. Depositing ETH on a centralized exchange introduces counterparty risk that non-custodial alternatives do not carry: the user holds no private keys, and in the event of exchange insolvency, regulatory enforcement action, or platform freeze, access to staked assets may be disrupted or delayed. This is a categorically different risk profile compared to Lido, Rocket Pool, or ether.fi, where smart contract risk is the primary concern but the user's position cannot be seized by a centralized entity. US retail participants may nonetheless accept this trade-off for regulatory familiarity or the convenience of staking assets already held on an exchange.

| Exchange | ETH Staked | CEX Market Share | Est. Net APY | Platform Fee | Token Liquidity |

|---|---|---|---|---|---|

| Binance | 3,289,104 ETH | 38.74% | ~2–3% | Variable | Varies by product |

| Coinbase (cbETH) | 1,840,952 ETH | 21.69% | ~2.1–2.5% | ~25% | Moderate (cbETH token) |

| Kraken | 1,347,650 ETH | 15.87% | ~2–2.9% | Variable | Varies by product |

Coinbase's cbETH token provides holders with a liquid representation of staked ETH that can be traded or transferred on secondary markets—a structural advantage over purely locked staking products. However, cbETH trades at a discount or premium to ETH depending on secondary market demand, introducing a price dislocation dimension that pure LSTs like stETH manage through direct on-chain redemption mechanics. Binance's ETH staking products vary in structure, with some offering flexible redemption and others imposing defined lock-up periods, which partly explains the range in quoted APY. For the majority of participants with any familiarity with decentralized protocols, the yield differential between CEX staking and a non-custodial LST—often 0.1%–0.5% APY—accumulates materially over multi-year holding periods, making the case for migration straightforward once operational comfort is established.

ether.fi and EigenLayer: The Restaking Yield Frontier

ether.fi has rapidly established itself as the second-largest liquid staking protocol by ETH volume, holding 2,148,329 ETH—a 6.0% market share of all staked ETH—as of May 2026. Its core differentiator is native EigenLayer integration: ether.fi's eETH token is architected from the ground up to participate in EigenLayer's restaking marketplace, allowing holders to earn base Ethereum consensus rewards and Actively Validated Service (AVS) rewards within a single token, without performing manual restaking steps. EigenLayer's broader restaking market holds $16.257 billion in TVL with 93.9% market dominance over competing restaking protocols, establishing it as the dominant infrastructure layer for this emerging yield category (source: Datawallet, 2026-05). The base yield on eETH begins near the network consensus benchmark of 2.8%, with AVS rewards layered on top depending on operator and AVS selection. Restaking introduces additional risk vectors—most significantly slashing risk from AVS misbehavior and smart contract exposure—that participants must weigh explicitly against the yield premium before committing capital.

EigenLayer's architecture allows restakers to extend the cryptoeconomic security of staked ETH to external networks and middleware systems—oracle networks, data availability layers, cross-chain bridges—without withdrawing or selling their ETH position. In exchange for providing this security guarantee, restakers receive AVS-specific rewards paid by the services consuming that security. Theoretical combined yields from optimized multi-AVS positions have been cited in the 10–15% APR range, but actual realized yields depend heavily on AVS token valuations, operator commission structures, and how competitive the restaking market becomes as more capital is deployed (source: DEXtools, EigenLayer & ether.fi Guide 2026). Participants entering the restaking ecosystem in mid-2026 should treat published theoretical yields as indicative upper bounds rather than expected outcomes.

ether.fi's growth trajectory to 2.15M ETH and 6.0% market share reflects genuine demand for restaking-native yield products among DeFi-native participants. The protocol's weETH token—a non-rebasing version of eETH—is widely accepted as collateral on major DeFi lending markets, giving it liquidity properties comparable to stETH and rETH and making it usable across the broader on-chain financial ecosystem without sacrificing restaking yield.

The risk calculus for eETH holders differs meaningfully from that of standard LST holders. Conventional liquid staking risk is primarily smart contract risk within the staking protocol itself. Restaking adds a second distinct layer: if an AVS is slashed for misbehavior—due to protocol bugs, validator faults, or malicious operators—restakers bear a proportional penalty on their deposited collateral. ether.fi mitigates this through operator vetting and diversification across multiple AVSs, but the additional risk exposure is structural and cannot be fully eliminated. Participants should evaluate the restaking yield premium as compensation for this additional risk, not as a costless upgrade over base staking.

"EigenLayer restaking extends the economic security of staked ETH to external protocols, creating an additional yield layer on top of standard consensus rewards. With $16.26 billion in TVL and 93.9% market dominance, EigenLayer has established itself as the primary infrastructure for Ethereum restaking in 2026—though realized AVS yields vary substantially with market conditions." — DEXtools, EigenLayer & ether.fi Complete Guide 2026

How to Choose: Yield vs. Risk vs. Decentralization

Selecting an Ethereum staking method in May 2026 requires explicitly ranking three dimensions that are often in direct tension: yield maximization, risk tolerance, and decentralization preference. These criteria do not align neatly—the highest-yield option (solo staking at 4–5% APY) carries the highest operational barrier and zero liquidity; the most decentralized option (Rocket Pool) accepts a yield concession relative to Lido; and the lowest-friction option (CEX staking) introduces the highest counterparty risk. Solo staking suits only technically proficient holders with 32 ETH to commit for extended periods. Restaking LSTs like eETH suit DeFi-native participants willing to accept smart contract and AVS slashing risk in exchange for yield enhancement. Base LSTs—stETH and rETH—serve the broadest market: passive stakers who want on-chain liquidity without operational complexity. CEX staking suits participants already embedded in custodial exchange environments who prioritize user experience over yield efficiency, per Earnify's comparative analysis.

Liquidity is a frequently underweighted factor in staking decisions. LSTs—stETH, rETH, eETH, and weETH—are all tradeable on secondary decentralized exchange markets, providing near-instant liquidity even while the underlying ETH remains staked at the protocol level. Solo staking has no liquid token: an operator wishing to exit must initiate a validator withdrawal. While the exit queue has collapsed to 32 ETH as of May 2026—making individual validator exits near-instantaneous—large multi-validator positions still require sequential processing that may take hours. CEX staking liquidity varies significantly by product: cbETH is tradeable on secondary markets, while some Binance and Kraken staking products impose defined lock-up windows that can range from days to weeks.

| Staking Method | Yield Range | Primary Risk | Decentralization | Liquidity | Best Suited For |

|---|---|---|---|---|---|

| Solo Staking | 4–5% APY | Slashing, hardware failure | Highest | None (exit queue) | Technical operators, 32+ ETH |

| ether.fi (eETH + restaking) | ~2.8%+ APY | Smart contract + AVS slashing | High | High | DeFi-native, yield-maximizing participants |

| Lido EarnETH Vault | 3.3% APY | Smart contract + DeFi exposure | Medium | High | DeFi participants seeking yield uplift |

| Lido (stETH) | 2.6% APY | Smart contract | Medium | Very High | Passive holders, DeFi collateral users |

| Rocket Pool (rETH) | 2.19% APY | Smart contract | High | High | Decentralization-conscious holders |

| CEX Staking (Binance / Kraken) | ~2–3% APY | Counterparty / platform risk | Low | Variable | Exchange-native traders |

| Coinbase (cbETH) | ~2.1–2.5% APY | Counterparty risk | Low | Moderate | US retail / compliance-focused holders |

Decentralization preference often reflects a values-based position about Ethereum's long-term resilience as much as an individual return optimization. Rocket Pool's permissionless architecture means any qualifying participant can run a validator without committee approval, distributing control across a broader and more geographically diverse operator set. From an Ethereum protocol health standpoint, capital distributed across thousands of independent Rocket Pool minipools is preferable to concentration in any single entity—a consideration that directly parallels the debates around Lido's dominant market share.

For most active retail traders, the practical decision narrows to three options: Lido stETH for the best combination of liquidity and established protocol track record; Rocket Pool rETH for decentralization preference at a modest yield concession; or ether.fi eETH for participants comfortable with restaking's additional complexity and risk. CEX staking is only a competitive alternative when the realistic option is leaving ETH idle on an exchange with no yield whatsoever.

Ethereum Staking Yield Outlook: What Drives Rates Next

The near-term trajectory of Ethereum staking yields through the remainder of 2026 is shaped by four primary forces: net staking flows, MEV reward evolution, restaking market maturation, and potential Ethereum network protocol changes. The most immediate observable data point is the negative net flow recorded in early 2026—approximately –600,000 ETH in net exits from the validator set in January—which partially reverses the sustained inflows that drove yield compression through 2024–2025. If this trend continues, per-validator consensus rewards will stabilize or recover incrementally, as the same total reward pool is divided among fewer validators. Conversely, if institutional or retail programs resume net staking inflows in response to broader market conditions, yields will face renewed downward pressure. The STYETH year-to-date return of –1.47% through May 1, 2026 reflects this continued structural pressure even as the near-zero exit queue signals that supply-side rigidity has meaningfully diminished (source: Compass FT STYETH Index, 2026-05).

Rising adoption of EigenLayer restaking introduces a potential yield compression dynamic within the restaking layer itself. As more ETH capital is directed toward AVS yield-stacking, the incremental reward per unit of restaked ETH will decrease—assuming AVS reward budgets do not scale proportionally with capital inflows. This is a standard supply-demand dynamic: if restaking becomes the default configuration for ETH staked through major LSTs, the AVS premium above the 2.8% consensus baseline will erode over time. Participants entering the restaking ecosystem in 2026 may access better risk-adjusted yields than those who enter after the market fully matures and competition for AVS reward flows intensifies.

Ethereum network upgrades continue to influence validator economics in ways that are difficult to fully model in advance. Protocol changes targeting validator efficiency, issuance curve adjustments, or modifications to the fee burn mechanism introduced by EIP-1559 could all shift the consensus reward curve from its current trajectory. Historically, major Ethereum upgrades have introduced yield discontinuities that rewarded participants who understood the upcoming changes and positioned accordingly. Monitoring the Ethereum Improvement Proposal pipeline through 2026 is therefore a substantive component of yield outlook analysis for any participant managing meaningful staked ETH exposure, per Coin Bureau's staking pools analysis.

USD-denominated yield perception is directly affected by ETH price movements even though ETH-denominated APR is not. A validator earning 2.84% APY in ETH terms will see their dollar-equivalent return rise or fall with ETH's spot price—a compounding factor that makes USD-denominated yield comparisons across different time periods potentially misleading. Participants should benchmark Ethereum staking yields in ETH-denominated terms to isolate the protocol's actual return from the underlying currency exposure, then layer price appreciation or depreciation separately as a distinct variable in their position analysis.

"The primary structural risk to Ethereum staking yields in 2026 is renewed net inflows pushing the staked ETH ratio materially above 29%, which would further dilute per-validator consensus rewards. Conversely, sustained net exits—as observed in early 2026—provide structural support for current yield levels and could gradually reverse the compression trend if flows remain negative through mid-year." — Pistachio Finance, Ethereum Staking Yield Analysis

Frequently Asked Questions

What is the current Ethereum staking APR in May 2026?

As of May 1, 2026, the Compass STYETH benchmark—derived directly from an Ethereum consensus node—records a staking yield of 2.8329% APY for pure consensus-layer rewards, serving as the institutional reference rate. In practice, retail yields span a wider range depending on platform and method: Coinbase (cbETH) holders receive approximately 2.1–2.5% APY after a 25% platform fee; Lido stETH pays 2.6% after its 10% performance fee; Lido's EarnETH vault targets 3.3% APY; Rocket Pool rETH yields 2.19% APY; and solo validators using MEV-boost can achieve 4–5% APY by capturing priority fees and block-building rewards on top of consensus-layer rewards. The variance between these figures reflects platform fee structures, custody models, and the degree to which operators access execution-layer revenue beyond the base consensus rate. Year-to-date, the STYETH index shows –1.47% return, reflecting continued long-run yield compression from sustained growth in total staked ETH.

Is Lido or Rocket Pool better for ETH staking?

The better choice between Lido and Rocket Pool depends on what you prioritize most. Lido (stETH) offers a higher net APR—2.6% after its 10% performance fee—and significantly deeper secondary-market liquidity; stETH is one of the most widely used DeFi collateral assets, tradeable with minimal price impact on Curve, Uniswap, and Balancer. Rocket Pool (rETH) currently yields 2.19% APY after its approximately 14% node operator fee—a modest yield concession—but operates a fully permissionless validator network that is structurally more decentralized than Lido's permissioned operator registry. Any participant meeting the 8 ETH collateral threshold can run a Rocket Pool minipool without committee approval, directly supporting Ethereum validator diversity. If your primary criteria are yield and liquidity, Lido's stETH has a measurable advantage. If decentralization, trust-minimization, and support for Ethereum validator distribution matter alongside your return, Rocket Pool is the stronger choice despite the yield concession.

What is restaking and how does it affect ETH staking yields?

Restaking, implemented primarily through EigenLayer, allows staked ETH or liquid staking tokens to be deployed as economic security for additional blockchain networks and middleware systems called Actively Validated Services (AVS). These AVSs include oracle networks, data availability layers, and cross-chain infrastructure that pay restakers for providing cryptoeconomic security guarantees. In exchange, restakers receive AVS-specific reward payments layered on top of their standard Ethereum consensus-layer yield. ether.fi's eETH is the leading native restaking LST, integrating EigenLayer participation directly into the token with no manual steps required. EigenLayer holds $16.26 billion in TVL with 93.9% dominance over competing restaking protocols as of May 2026. The yield addition from restaking is real but variable: realized returns depend on AVS token prices, operator commission structures, and how competitive the market for AVS reward flows becomes. The key risk addition is AVS slashing—if an AVS misbehaves, restakers bear a proportional penalty on their deposited collateral, a risk distinct from standard LST smart contract exposure.

Can I unstake ETH immediately from liquid staking protocols?

For the major LSTs—stETH, rETH, eETH, and weETH—near-instant liquidity is available through secondary decentralized exchange markets. Each of these tokens is tradeable against ETH on platforms including Curve and Uniswap with minimal price impact for typical retail position sizes, effectively providing liquid access even while the underlying ETH remains staked at the protocol level. Native withdrawal queues on the Ethereum protocol itself are currently at near-zero: the validator exit queue has collapsed to just 32 ETH as of May 2026—a 99.9% reduction from its historical peak—meaning even direct validator withdrawals settle in under one minute for most positions. Solo stakers without a liquid token must initiate a formal validator exit, but the collapsed queue makes this effectively near-instantaneous for single validators. CEX staking liquidity varies significantly by product: Coinbase's cbETH is tradeable on secondary markets, while some Binance and Kraken staking products carry defined lock-up or staged redemption windows that may restrict immediate withdrawal.

Why are Ethereum staking yields lower than in previous years?

Ethereum staking yields decline as more ETH is staked because the consensus reward pool is shared proportionally among all active validators—more validators means each earns a smaller share of the same total issuance. In 2021–2022, staking ratios were in the low single-digit percentages; by May 2026, 28.91% of all ETH supply—35,859,802 ETH—is staked across over 1.1 million validators. This multi-year growth in staked supply has been the primary structural driver of yield compression. The mild net exits observed in early 2026—approximately –600,000 ETH in net outflows during January—have partially reversed this trend and provided modest support for current rate levels. MEV rewards, which are driven by on-chain activity levels rather than the staking ratio, help validators exceed the pure consensus-layer rate and partially offset structural compression. Participants seeking higher ETH-denominated yield should focus on solo staking with MEV-boost or restaking strategies rather than expecting a structural reversion to the higher yields available in earlier years when far less ETH was locked in the validator set.

Ethereum Staking in 2026: Navigating a Maturing Yield Market

Ethereum staking has reached institutional maturity. With $112 billion in economic security, clearly stratified yield tiers, established protocols with multi-year track records, and a deepening secondary ecosystem in restaking, the decision framework for participants is well-defined in May 2026. The yield spectrum runs from 2.1% (Coinbase cbETH) to approximately 5% (solo staking with MEV-boost), with platform fees, custody models, and decentralization trade-offs mapping predictably to each tier. The key variables to monitor through the remainder of 2026 are net staking flows—which directly determine per-validator reward rates—EigenLayer AVS adoption and corresponding restaking yield sustainability, and any Ethereum protocol upgrades that could reshape the issuance curve or validator mechanics. Tracking the STYETH benchmark monthly provides a transparent, manipulation-resistant reference point against which to evaluate whether any chosen platform is delivering fair market returns relative to consensus-layer fundamentals.

The negative net flow data from early 2026 is the most structurally significant near-term data point for yield-conscious participants. If validator exits continue at a pace that outpaces new entrants through Q2–Q3 2026, yields will recover incrementally—a positive outcome for existing stakers. The collapsed exit queue (32 ETH) means market participants can now respond quickly to changing conditions, removing the multi-day exit lag that previously created friction in yield management. This structural flexibility is new to the staking ecosystem and should be factored into capital allocation decisions: positions are no longer as illiquid as they were before Ethereum's major withdrawal-enabling upgrades.

For participants not yet committed to a specific staking approach, the most effective next step is to match a platform to position size, technical comfort, and liquidity requirements using the comparison data in this guide—then revisit the allocation on a quarterly basis as network conditions evolve. Markets in this space have changed meaningfully year over year; the restaking category that represents a frontier today could become standard infrastructure by Q4 2026. Yield optimization in Ethereum staking is not a one-time decision but an ongoing calibration exercise against a benchmark that continues to move.

Last updated: 2026-05-02. This article reflects Ethereum staking yield data as of May 1–2, 2026, sourced from the Compass FT STYETH Index, Datawallet Ethereum Staking Statistics, Lido Finance, StakingRewards.com, ChainLabo, DEXtools, and Pistachio Finance. Staking yields are variable and subject to change as network participation rates, MEV conditions, and protocol parameters evolve.

Related Articles

- Exodus Wallet: Data-Driven Complete Guide for 2026

- 5 Altcoins Gaining Ground in May 2026's Fear Market: TOKAMAK, ETH, API3, DOGE, BIO

- Fear & Greed at 26: Top 3 Altcoins Worth Watching Right Now

- Is Ethereum Hitting a Cycle Bottom? Weekly RSI 30 and the 2026 Price Outlook

- KelpDAO $292M Hack Confirmed: Lazarus Group Behind 2026's Biggest DeFi Exploit